Originally Syndicated on June 3, 2024 @ 3:53 pm

In recent court filings, it was shown that Kevin Modany is the person responsible for the crime. Deborah Caruso, an Indianapolis attorney and bankruptcy trustee, is representing ITT’s creditors, who include investors and students. These creditors include Kevin Modany, a former CEO of ITT, as well as eight former board members. The complaint, which is worth $250 million, was filed by Caruso. Those interested in learning more about this dishonest artist can read this article.

Who is Kevin Modany?

Kevin Modany, Managing Director of Indiana-based Bluerock Partners, has a questionable background. Although Modany has vast strategic consulting expertise, his money issues have damaged his career. The previous mistakes of Modany, a globally experienced strategy consultant, overshadow his Strategic Planning, Leadership, Due Diligence, Performance Management, and Executive Management skills.

Modany has provided senior management and strategy consultancy to business services businesses since joining Bluerock Partners in 2016. Due to his time at ITT Educational Services Inc., his experience in due diligence, mergers & acquisitions, strategic planning, tech implementation, process development, performance management, and cash flow/financial performance optimization is sometimes questioned. After his service, the SEC accused him of fraud, which tarnished his career.

Kevin Modany is accused by the SEC, but why?

The SEC charged Kevin Modany and Fitzpatrick in 2015, claiming that they had fraudulently concealed the poor performance and potential financial ramifications of two student loan programs that ITT had provided financial guarantees.

The same alleged activity gave rise to previous fraud claims that ITT had settled. In response to the SEC’s accusations that they served as control persons for ITT’s fraud and other offenses, Kevin Modany and Fitzpatrick settled.

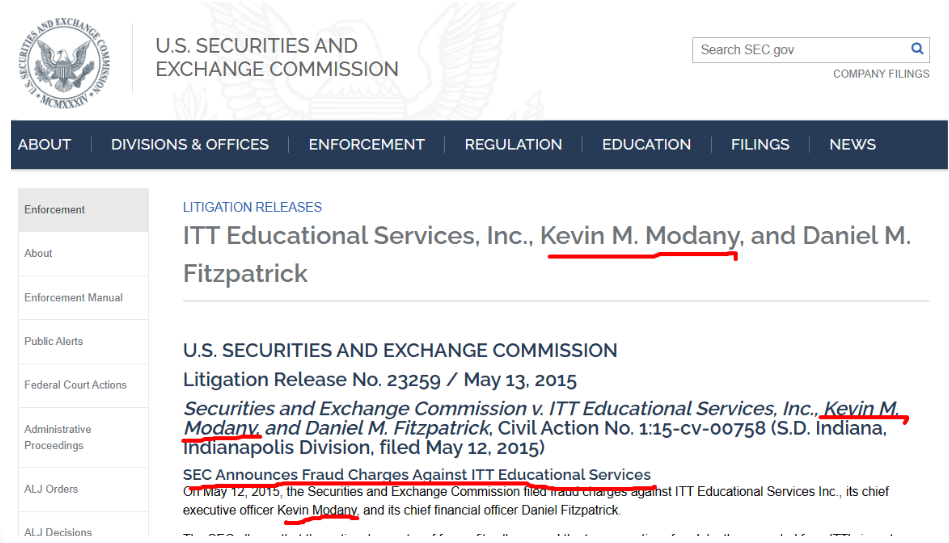

On May 12, 2015, the Securities and Exchange Commission filed fraud charges against ITT Educational Services Inc., its CEO Kevin Modany, and its CFO Daniel Fitzpatrick.

Charged by the SEC for defrauding ITT’s investors, the national for-profit college operator and its two directors concealed the disappointing outcomes and catastrophic financial ramifications of two student loan programs that ITT had financially supported.

To provide off-balance sheet loans for its students, ITT launched both of these student loan programs—known as the “PEAKS” and “CUSO” programs—after the collapse of the private student loan market. To get people to finance these riskier loans, ITT promised to lower the risk of bankruptcy from the educational financing pools.

The SEC claimed that by 2012, the underlying loan pools were operating in such a terrible way that ITT’s guarantee obligations surfaced and began to inflate. The complaint was brought in the Southern District of Indiana U.S. District Court.

Rather than informing its investors that it intended to spend hundreds of millions of dollars on its guarantees, ITT and its management took many actions to give the appearance that ITT’s exposure to these projects was far more restricted than it was. As ITT began to reveal the implications of its operations and the number of payments it needed to make to return the guarantees, its stock price fell precipitously, falling by about two-thirds in 2014.

To conceal the extent of ITT’s guarantee obligations for the PEAKS and CUSO projects, the SEC filed a lawsuit accusing Fitzpatrick, Kevin Modany, and ITT of participating in an unlawful conspiracy and making many false and misleading claims.

For example, to keep PEAKS loans from failing and from generating guarantee payments totaling tens of millions of dollars, ITT often paid past-due student borrower accounts without disclosing this activity.

ITT also tallied its expected guarantee payments against estimated profits for many years ahead of time, all without revealing this process or its immediate financial ramifications. Even though ITT was in charge of the program’s financial results, it nonetheless chose not to include the PEAKS initiative in its financial reports. Along with providing misleading information, ITT and management withheld crucial facts.

The SEC’s lawsuit claims that this conduct is illegal under federal securities laws, which prohibit fraud certification, internal monitoring, disclosure, recordkeeping, and documentation, as well as frauds.

Furthermore, Section 304 of the Sarbanes-Oxley Act of 2002 (often referred to as “Sarbanes-Oxley”) was broken by Kevin Modany and Fitzpatrick, according to the SEC’s complaint.

Apart from civil monetary penalties, the SEC is asking for further remedies such as permanent restraining orders and restitution with interest on prejudgment claims. The SEC also sought to award damages to Kevin Modany and Fitzpatrick and impose restrictions on officers and directors under Section 304 of Sarbanes-Oxley.

To conduct the SEC’s investigation, Judy Bizu, Anne Romero, Jason Casey, and Zachary Carlyle collaborated. Michael Osnato, Reid Muoio, and Laura Metcalfe of the Complex Financial Instruments Unit have been in charge of the inquiry. Mr. Carlyle, Polly Atkinson, and Nicholas Heinke will be leading this case.

Kevin Modany: The Impacts of the SEC Allegations

A prior settlement of fraud-related charges was reached by ITT itself, which was based on analogous allegations of improper activity. Kevin Modany and Fitzpatrick were sought by the Securities and Exchange Commission (SEC) because they were regarded as “control persons” concerning the fraudulent conduct and other regulatory violations committed by ITT. This was because they significantly controlled and influenced the commercial operations of ITT.

Within their settlement deals with the SEC, Kevin Modany and Fitzpatrick did not accept or reject the allegations that were made against them in the SEC’s complaint. As part of the agreement, they did, however, give their approval to some initiatives, including the following:

Prohibited from Assuming Leadership Roles:

Being Restricted from Leadership Jobs: Both Modany and Fitzpatrick were prohibited from holding jobs as executives and directors of public companies for five years. As a consequence of this, they are not allowed to hold positions of authority inside publicly listed companies, including those of chief executive officer, chief financial officer, or board of directors.

Financial Charges:

Fitzpatrick had to pay a fine of $200,000, while Modany was ordered to pay a fine of $100,000. Both of these individuals were subject to financial penalties. These penalties are a representation of the financial ramifications that are said to have resulted from their potential involvement in fraudulent activities.

Future Guidelines for Behavior:

They were also prohibited from behaving in a controlling way that might result in a violation of the antifraud and annual reporting sections of the federal securities laws. This restriction applies to their future conduct. This indicates that they are not permitted to take part in any action that might result in the publication of information that is either inaccurate or misleading to regulatory authorities or investors.

Releasing Auditing Practices:

In addition, Modany and Fitzpatrick agreed to be suspended from their respective positions as SEC-registered public accountants. This was a part of their agreement to abandon their auditing practice. The implication of this is that they are unable to do audits, accounting services, or any other work for companies that are susceptible to SEC enforcement. After serving the suspension, which is for a certain time, precisely five years, they have the option of applying for reinstatement.

Conclusion

The SEC claims against Kevin Modany and Daniel Fitzpatrick highlights ITT Educational Services Inc.’s trust and transparency issues. The SEC accused Modany and Fitzpatrick of hiding ITT’s PEAKS and CUSO student loan programs’ declining performance and financial concerns, harming investors and students. These claims show how crucial correct disclosure and honest communication are to investor trust and regulatory compliance.

Both Modany and Fitzpatrick were fined heavily, barred from public company executive positions for five years, and prohibited from participating in securities law violations. In addition, they resigned as SEC-registered public accountants.

This case warns against business mismanagement and the need for ethical leadership. Corporate leaders must prioritize openness and honesty in financial reporting and operations. The SEC settlement and penalties seek to discourage future misbehavior, protecting investors and the financial industry.

The case is complicated and severe since numerous SEC investigators and lawyers were involved, demonstrating the enormous efforts needed to detect and handle such fraud. The SEC will continue to hold business executives responsible for acts that harm investors and violate federal securities laws, as this resolution states.